On 24 February 2026, Azalea hosted Astrea Investor Day 2026, our annual forum for Astrea Private Equity ("PE") bond investors, to share updates on the Astrea platform, market developments, and the performance of the Astrea PE bonds.

Building on our ongoing commitment to investor education, this year’s session also featured a dedicated segment on private equity secondaries – a strategy that plays a central role in the Astrea programme.

Azalea Overview

Lim Jun Jie, Head of Investor Relations, opened the session with a firm overview of Azalea and our mission to broaden access to private equity, including retail investors. Established in 2015, Azalea has continued to grow steadily and today manages approximately US$14 billion in assets. Across the Astrea and Altrium platforms, Azalea serves more than 80,000 individual investors and over 200 institutional investors, supported by a team of more than 70 professionals.

Reflecting on the past year, Jun Jie shared several key milestones – including the successful launch of Astrea 9 in August 2025, the largest Astrea offering to date, and the continued strong performance of existing Astrea issuances. All Astrea bonds have continued to meet their bond obligations, even through periods of market volatility, reflecting the robustness of the Astrea structures and the resilience of the underlying portfolios. Azalea is also expected to hold its final close for Altrium Private Equity Fund III, its flagship PE fund-of-funds programme, in the first half of 2026.

Market Update

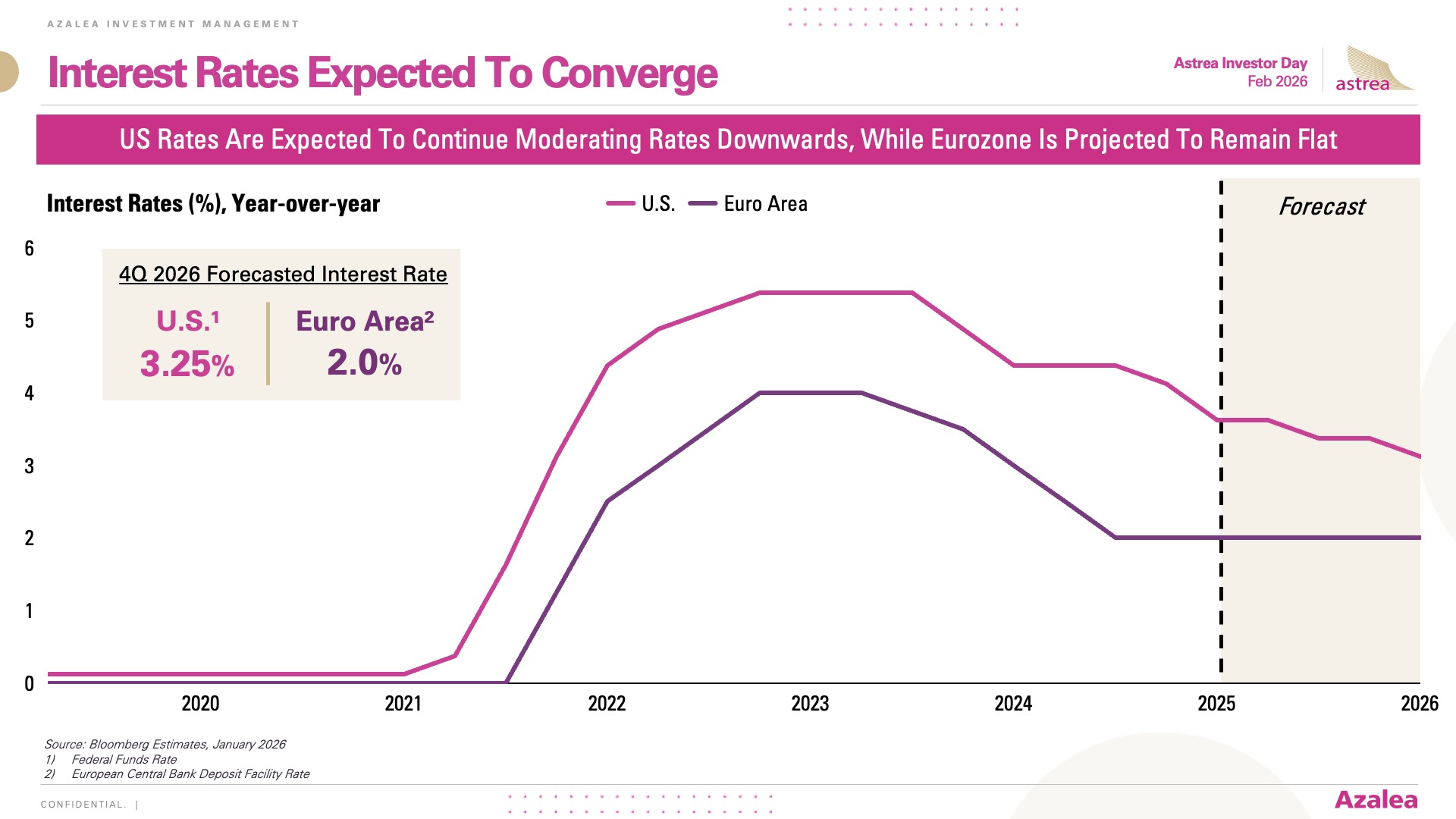

Justin Keh, Managing Director, Investments, highlighted several key market updates. He highlighted how global markets have navigated an environment of recurring political and geopolitical headlines. While headline-driven volatility continues to be seen, market reactions have increasingly been sharp but short‑lived, with capital markets remaining open and transactions continuing to take place.

Justin also shared that global economic growth has remained relatively stable, supported by services activity, technology investment and fiscal measures in major economies. Inflation has moderated from prior peaks, although progress has been uneven across regions, contributing to diverging interest rate paths. Encouragingly, early signs of recovery have also emerged in the private equity exit environment, supported by stabilising interest rates and improved price discovery, which are important for distributions, portfolio rebalancing, and capital recycling across the PE ecosystem.

Understanding Secondaries in Private Equity and Astrea

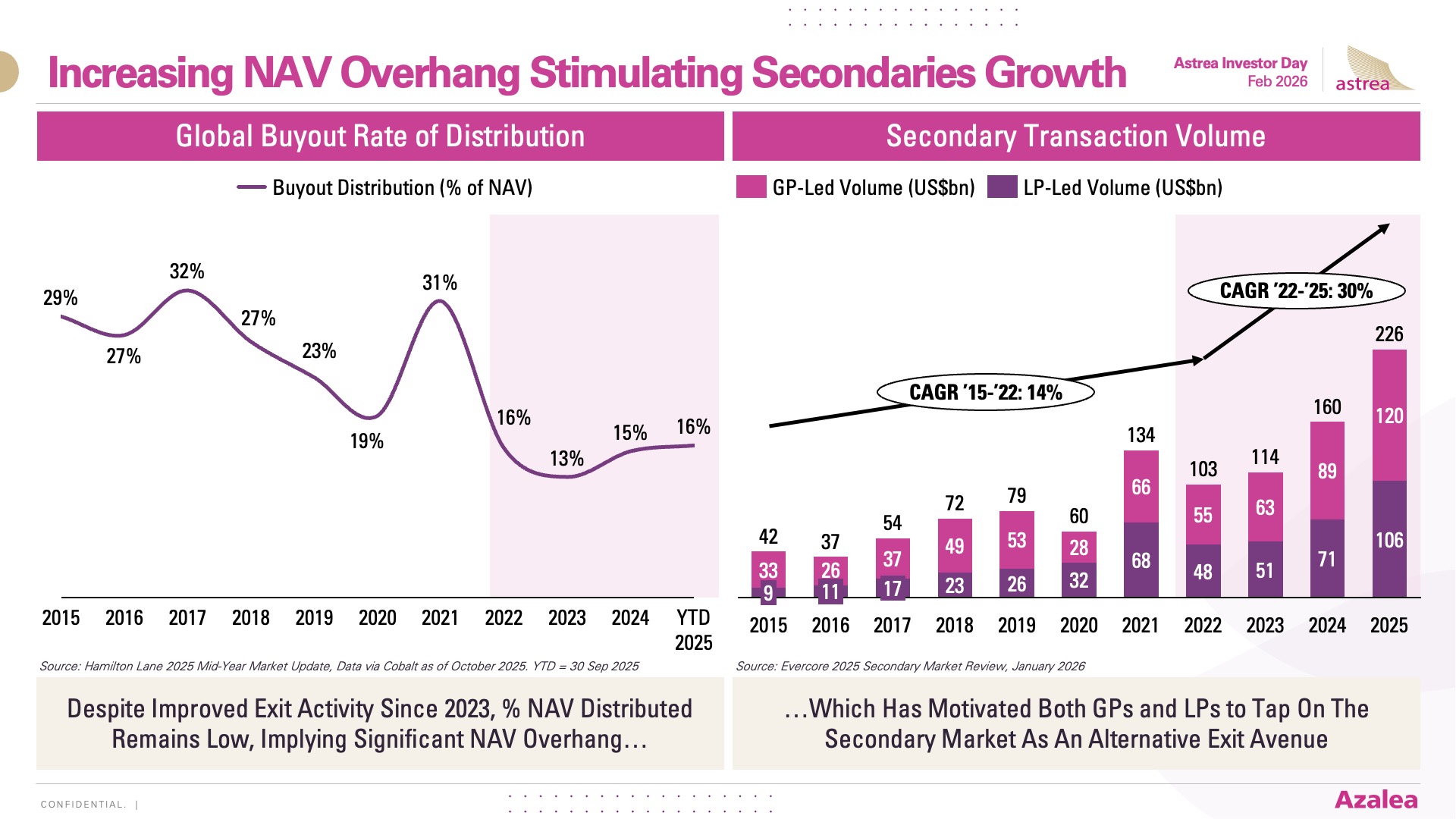

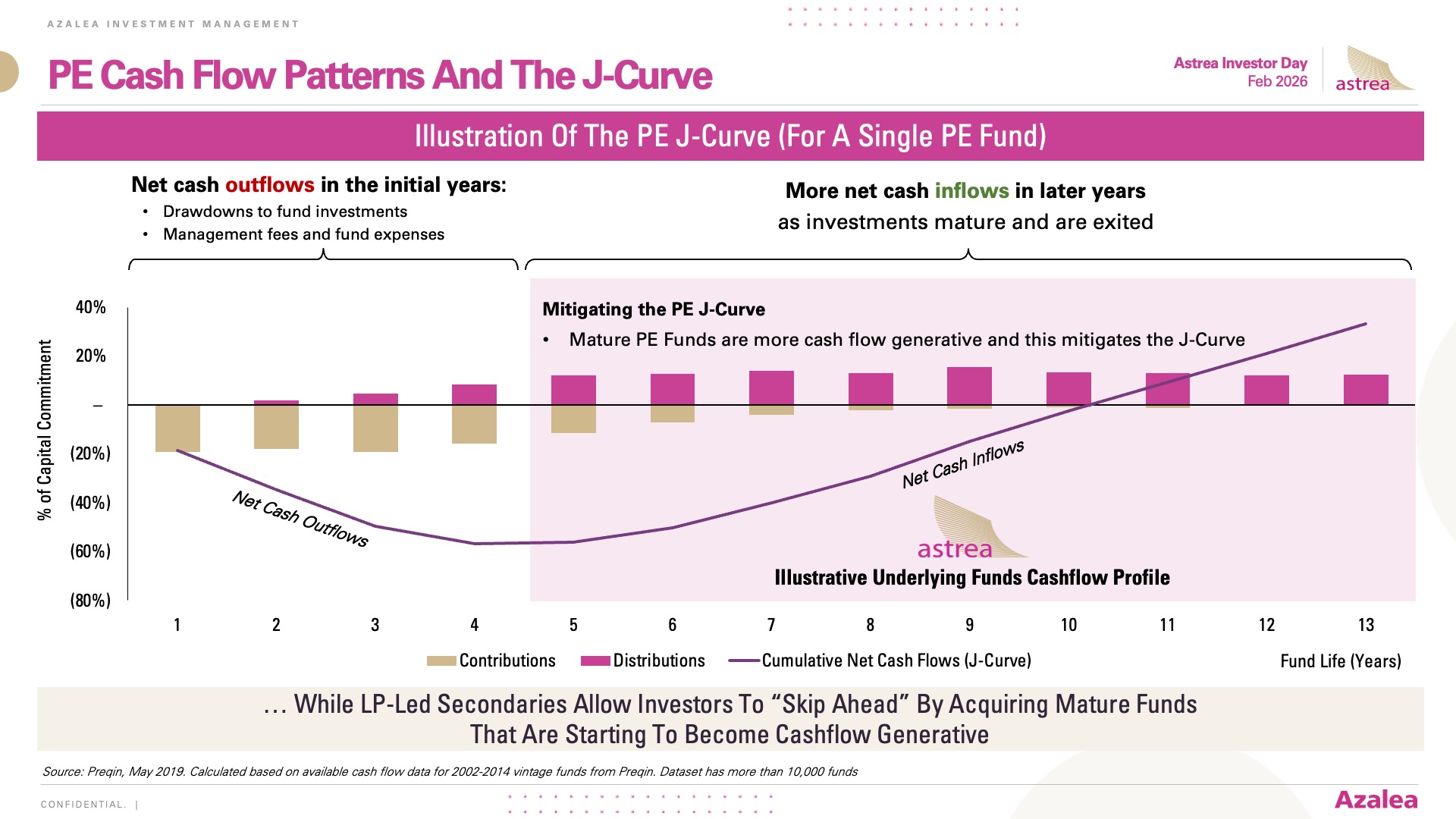

A key focus in the 2026 edition was an educational deep‑dive into private equity secondaries – a rapidly growing part of the PE market and a key strategy in the Astrea platform. The session explored how private equity funds operate, recent challenges in distributions across the industry, and how these dynamics have contributed to the growth of the secondary market as investors seek liquidity solutions.

The discussion covered both Limited Partner (“LP”)‑led and General Partner (“GP”)‑led secondary transactions, with a focus on why Astrea is fundamentally an LP‑led strategy. By acquiring mature private equity portfolios that are typically further along their life cycle, Astrea portfolios are generally more cash‑generative, supporting the payment of bond obligations.

The diversification, asset visibility and shorter duration exposure associated with secondaries were also highlighted as key structural strengths.

Astrea Performance Updates

Jun Jie then shared updates on the performance of the various Astrea transactions.

- The Astrea VI portfolio has enjoyed strong cash distributions since issuance, totalling over US$1.3 billion, which represents approximately 92% of the starting portfolio Net Asset Value (“NAV”). The Class A Bonds have been fully reserved as of March 2025 and are on track to be fully redeemed as per scheduled in March 2026, five years after issuance

- The Astrea 7 portfolio has enjoyed strong cash distributions of more than US$1 billion, around 53% of the starting portfolio NAV. As of the last Distribution Date, the Reserves have been on track and accumulated to around 75% of Class A Bonds size, while the Loan-to-Value ratio (“LTV”), sits comfortably at 27.3%, below the 50% Maximum LTV ratio

- The Astrea 8 portfolio has generated cash distributions of over US$360 million, about 25% of the starting portfolio NAV, which has been more than enough to satisfy bond obligations to date. As of the last Distribution Date, the Reserves Amount is around 40% of Class A-1 Bonds size and the LTV ratio remains healthy at 34.5%, below the 50% Maximum LTV ratio

- Issued in August 2025, Astrea 9 is the latest addition to the Astrea platform and marked a milestone, being the largest retail offering thus far. The portfolio has generated healthy cash distributions of US$188 million, or about 12% of the starting portfolio NAV. As of the last Distribution Date, the Reserves Amount is around 11% of Class A-1 Bonds size and the LTV ratio of Class A Bonds remains healthy at 38.4%, below the 50% Maximum LTV ratio

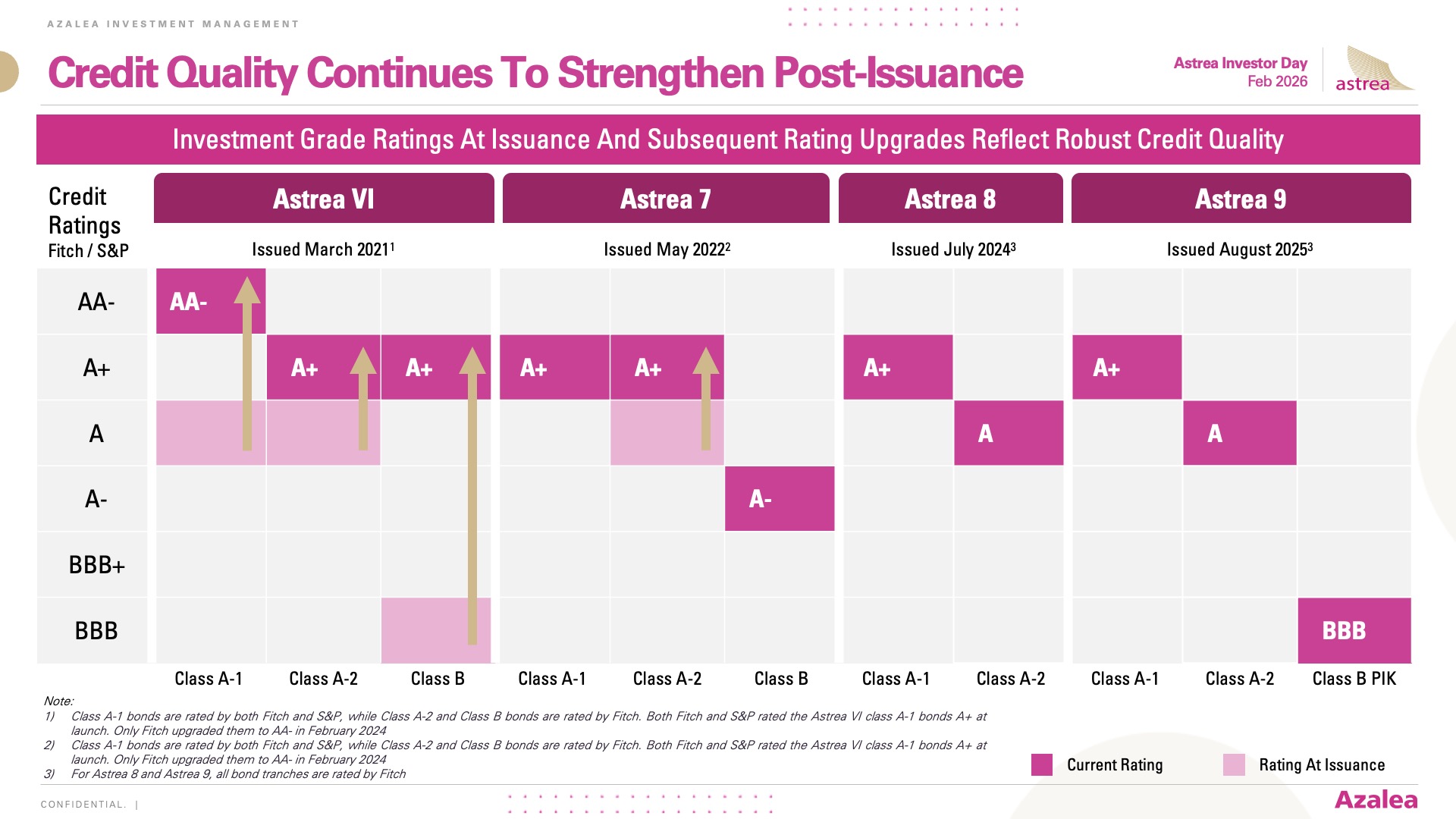

Jun Jie also highlighted the credit strength of the Astrea PE bond series which saw multiple credit rating upgrades over the years. He also shared that the Astrea portfolios continued to be cash generative, which helped to de-risk Astrea transactions progressively over time.

Key Takeaways

Jun Jie closed off the presentation by highlighting several takeaways from the Astrea Investor Day 2026.

- Stable growth, easing inflation: Economic growth remains stable in 2025, with inflation expected to moderate further in 2026

- Resilient market conditions: Markets continue to demonstrate resilience amid ongoing geopolitical and political volatility

- Secondaries as the core of Astrea: Private equity secondaries remain the foundation of the Astrea programme.

- Strong portfolio fundamentals: Astrea portfolios provide diversification and liquidity characteristics similar to secondary fund‑of‑funds strategies

- Cash‑generative portfolios supporting bond obligations: All Astrea portfolios continue to reserve on schedule and generate sufficient cash flows to meet bond obligations

Disclaimer: Please note that all information shared in this session is intended for your information only and is not an offer, invitation, or recommendation to purchase, hold or sell any securities. If you would like to receive any investment advice or recommendation, please do speak with a qualified financial advisor.

Watch the recording of the presentation here: